Reporting Cryptocurrency Transactions at Tax Time

Have you dived into the world of cryptocurrency exchanges?

Cryptocurrency is used to describe encrypted virtual currencies which exist as digital tokens. This digital currency operates outside of government via decentralised ledgers or digital wallets but can be exchanged for online goods and services.

The ATO treats cryptocurrency as a form of barter exchange. There is no problem with exchanging goods and services so long as the transactions are recorded and valued correctly.

Business or Personal?

Whether it’s business or personal, crypto exchanges (buying, selling or holding crypto assets) are subject to the same income tax and GST treatment as cash or credit transactions.

If you use cryptocurrency in your business, you’ll need to account for cryptocurrency just as you would for other business transactions. If you’ve used it for personal investment, you’ll need to include details in your income tax return.

The ATO uses data supplied by Australian cryptocurrency exchanges, state revenue offices and shares data to cross-reference the crypto gains and losses information in your tax returns.

Crypto Transaction Records

Keep records of all transactions, including dates, AUD value, the nature of the transactions, exchange receipts, legal costs and other parties involved (even a crypto address is enough) in the sale or purchase of cryptocurrency.

Cryptocurrency and the ATO

The ATO has taken a lenient approach to pursue taxation of crypto assets. However, now that cryptocurrency is attracting more mainstream investors and there is a lot more data available, the ATO checks the taxation obligations of individuals and businesses with crypto assets.

There are different rules for using cryptocurrency in business and for personal expenses or investment. Business transactions use the trading stock rules, while private exchanges involve capital gains tax rules.

Talk to us. We’ll check that all your crypto transactions are recorded correctly for your tax return. Don’t get caught out by the ATO spotlight on cryptocurrency at tax time!

Tax Tips for Individuals

Are you making the most of allowable tax deductions? Individuals can claim for general work-related expenses as well as occupation-specific expenses and working from home. Book a time now to prepare your 2021 tax and we’ll help maximise your return.

Get ahead now by preparing all the documents required for your 2021 tax return so you can get your tax done quickly and get any refund due to you in your bank!

Income

The Australian Taxation Office (ATO) automatically receives information from your employers about salary and wages that you have been paid for the financial year. You need to declare all income from other sources on your tax return as well.

- Wages, salaries, allowances or bonuses from all employers.

- Pensions, annuities or government payments such as JobSeeker or JobKeeper.

- Investment income including interest earned and dividends paid.

- Business income, if you have a business as well as a job.

- Foreign income.

- Crowdfunding income.

- Sharing economy income such as Uber or Airbnb.

- Income such as hobbies, prize money, compensation or insurance payments may be tax free but check with us.

Even if you have only earned a small amount from one of these sources, it still needs to be declared on the tax return. Gather all your records for anything you have earned apart from salary and wage payments from employers.

You will need:

- bank statements that show interest income;

- proof of earnings from other sources such as crowdfunding or share economy platforms;

- records of business or hobby income;

- records of government payments received;

- and records of any other payments received from overseas sources, prize winnings, insurance or investments.

Tax Deductions

Have you captured all your work-related deductible expenses to make the most of your 2021 tax return?

Employees are entitled to claim work-related expenses as a tax deduction. To claim a deduction, you must have spent the money out of your own funds and not have been reimbursed by your employer. The expenses must relate to your earnings as an employee. Make sure you have invoices and receipts as proof of payment for any work-related expenses.

Expenses you may be able to claim

- Vehicle and travel expenses – use a travel diary to record details of trips taken for your employment.

- Clothing, laundry and dry-cleaning expenses – you can claim for occupation specific clothing, uniforms and protective gear.

- Home office expenses – there are special rules this year for employees working from home because of COVID-19. You will need records of the hours you have worked from home to claim the ATO special rate.

- Self-education expenses – some education expenses that relate to your current employment are claimable.

- Tools and equipment – if you buy gear to help you in your job, this may be claimable. Small tools of trade, protective items, professional references and laptops are some examples of equipment you may be able to claim.

Occupation and Industry Specific Guidelines

The ATO recognises that some occupations and industries have specific requirements that employees need to pay for.

There are handy ATO fact sheets for many industries, including hairdressers, teachers, performing artists, hospitality workers, lawyers, medical professionals and more.

These guides are a great starting point if you are not sure what you can claim, but we can give you information tailored to your situation when you do your tax return with us.

Superannuation

If you have made personal superannuation contributions separate to your employer’s superannuation guarantee contributions, you may be able to claim this as a tax deduction. You will need to provide a notice of intent to claim form to your super fund and receive acknowledgement from the fund before doing your tax return.

Book a time with us now to prepare for your tax return and we’ll make sure you make the most of all applicable tax deductions this year.

Income Splitting – New Rules from July 2021

Are you interested in learning more about income splitting and how to minimise tax by apportioning income or profit between associated entities?

Professional services firms frequently use income splitting – for example, medical, legal, financial or IT services firms. It’s a good way of reducing tax within the allowable provisions – so long as it is not stepping over the boundary into tax avoidance.

New ATO guidance on this topic means individual professional practitioners (IPP) will need to prove that arrangements are commercially motivated before self-assessing the risk level of current income splitting arrangements.

The new guidelines will apply from 1 July 2021 and are more involved than the guidelines currently used to satisfy the ATO’s requirements.

The ATO will be on the lookout for arrangements that result in payments to an individual that seem to be artificially low due to income splitting in order to avoid tax.

In assessing the risk of tax avoidance, the ATO takes into account several factors:

- The proportion of profit entitlement from the whole of the firm that is returned to the IPP.

- The total effective tax rate for income received from the firm by the IPP and associated entities.

- The remuneration returned to the IPP as a percentage of the commercial benchmark for the services provided to the firm.

Talk to us about income splitting arrangements and how they can benefit you within the rules.

We’ll work through the new guidelines with you to assess the commercial rationale of arrangements and any high-risk features that may trigger an ATO audit. If you’re thinking of restructuring operations, now is the time to review existing arrangements.

Reach out to the team at Solve Accounting today!

NSW Government Grants for Businesses

The Prime Minister and NSW Premier has announced an expanded support program for NSW business affected by this current lockdown. This is welcomed as we know many clients and individuals who are struggling financially due to the restrictions.

The package includes a number of support measures, for which businesses will be able to apply from Monday 19 July 2021:

- The extension of the existing NSW Business Grants package for a third lockdown week. The NSW Government grants are available for businesses, sole traders and not-for-profit organisations impacted by the restrictions. You can receive a grant of between $7,500 to $15,000 depending on decline in turnover experienced.

- A cash boost for businesses across NSW with an annual turnover of between $75,000 and $50 million which can demonstrate a 30% reduction in this turnover during lockdown. The cash boost will be 40% of weekly payroll with a payment of between $1,500 to a maximum of $10,000 per week from week 4 of lockdown onwards, provided staffing levels are maintained.

- $1,500 fortnightly grants for micro businesses with turnover of between $30,000 and $75,000 which can demonstrate a 30% reduction in turnover where the business is the primary source of income.

- A payroll tax deferral this quarter for all businesses, and a waiver for this quarter if you can demonstrate a 30% reduction in turnover and you have a payroll of between $1.2 and $10 million.

- Increase in the payment amount for stood down workers from $500 to $600 per week for those who lost more than 20 hours, and to $375 for those who lost between 8 and 20 hours, and for it to be available to workers outside of Sydney lockdown areas.

- Several provisions around residential, commercial and retail leases, including no lockouts and forced evictions, and those landlords who provide rent relief will be given land tax reduction incentives.

Applications for the “Business Grant” are open today. Applications for “JobSaver” and “Micro Business Grant” are not yet open but should be available within the next week.

Here’s what you can do to prepare for your grant application:

- Calculate your decline in turnover – you need to compare a 2-week period within 26 June 2021 to 17 July 2021, to the equivalent period in 2019.

- Confirm your turnover for the year ended 30 June 2020 – the key threshold is whether you are above or below $75,000 (and under $50m).

- If you are an employer, confirm your employee headcount as at 13 July 2021 (permanent employees and casuals that have been employed for more than 12 months)

- Create a MyServiceNSW Account for your business (if you do not have one), and ensure your details are up to date.

- If you meet the eligible criteria as outlined by Service NSW, please apply online and follow the steps.

- Maintain records of supporting documentation as outlined by Service NSW for each grant application for up to 5 years in the event of an audit.

Please visit https://www.service.nsw.gov.au/campaign/covid-19-help-businesses/grants-loans-and-financial-assistance for more details and information around eligibility and how to make a claim.

Please contact us if you need assistance with your grant applications or to confirm your eligibility. The team at Solve Accounting are here to support you through this challenging period.

Advanced tax strategies for high-income earners in Australia

Even with COVID and the incentives provided by the Australian government, there are still genuine concerns from high-income earners and their taxable income, because tax laws make it so that high-income earners get taxed at the highest rates.

It’s never too late to focus on tax deduction strategies that can result in you paying fewer taxes.

Why is Tax Planning Important?

It improves income flow and leads to greater flexibility

When you take the right steps in your tax bracket, you’ll be able to keep more money flowing to your household and lower tax payable to the ATO. This could possibly save you thousands of dollars per year and allow you to focus your finances on other important areas without digging into your savings.

You can take advantage of all the deductions and exemptions

If you’re not well-versed in tax affairs, you might miss out on a few available allowances, deductions, and exemptions. A reliable tax accountant would be up to date with any recent changes, and let you know when and how to take advantage of these concessions when completing your tax refund.

You remain compliant and current

When it comes to tax planning, many individuals like to take the safer course of action as the last thing they want to appear like they are conducting tax evasion or dodgy practices. A tax accountant can look for opportunities within the tax compliance boundaries and provide you with the tax deduction advantages it needs to improve when completing your tax return.

The below tips are ways to reduce your tax, include the general tax tips and more advanced tax return tips that would also cover high net worth individual taxpayers and sophisticated investors.

1. Make personal super contributions

Making personal contributions from free cash flow (salary sacrifice) each year is an effective way to both reduce your tax bill and increase your retirement savings. You are able to contribute up to $25k each year (including contributions made on your behalf by your employer). Individuals with a taxable income of between ~50k and $250k tax brackets gain the most from this strategy due to the super tax rate (15%) versus your marginal tax rate.

2. Main residence

The main residence capital gains tax concessions are arguably the most valuable tax break in Australia for building personal and family wealth. If you are able to invest in property, ensure you make it your main residence once it’s acquired. If circumstances change you are able to move out and rent the property for up to 6 years whilst continuing to treat it as your main residence for tax purposes. Expats should be aware of recent changes to these rules which make them less tax concessionary for such individuals, however, these risks can be managed.

3. Negative Gearing

“Negative Gearing” means generating investment losses (generally due to interest costs) which can be written off against your salary/wage income to create a tax refund. Negatively gearing a property or share portfolio is a tax-efficient strategy where you expect the investment to go up in value in the long-term. The long-term gain in value is generally a capital gains tax on future sale (at concessional rates), whilst in the short-term, the tax refunds can assist in funding the losses. Key to negatively gearing is ensuring the investment pays an income stream to make the interest tax deductible. Always obtain advice prior to investing to ensure the interest is deductible!

4. Franking Credits

“franking credits” are attached to most dividends you receive from Australian share investments. Franking credits are unique compared to other “tax offsets” in that they can give rise to a cash refund where they are greater than the amount of tax you owe for the year. The tax benefit of franking credits is magnified in a self-managed super fund environment due to the tax rate in super only being 15%.

5. Home office expenses

As workplaces become increasingly flexible with WFH arrangements, all eligible individuals should be claiming home office expenses. You have a choice of keeping records and claiming deductions for using your home as an office or “place of convenience” to undertake work. The ATO has provided a “shortcut” method for calculating home office expenses due to COVID-19 for the first half of FY21, so ensure to keep records of hours worked at home for this period.

6. Keep a car logbook

For anyone who travels for work-related purposes (e.g. to/between clients or workplaces), please keep a 12-week logbook of your most busy travel period. This can then be used to calculate your deductible percentage of your car expenses for the financial year. This can give you a better outcome than the “cents per kilometre” method, which is often the default in the absence of good records. Keeping a logbook during the year gives you the option of a more favourable method to maximise your car deductions at tax time.

Make personal deductible superannuation contributions before (say) 25 June to ensure the cash is received by the fund before 30 June – for tax savings and co-contribution purposes

7. Deferral OR bring forward of bonus income

Ask your payroll manager to pay any bonuses on 1 July instead of before 30 June IF you anticipate less income next financial year & vice versa (pregnant women, women planning pregnancy and taking maternity leave in 2020, returning expats with carried forward losses, taxpayers planning a step-down job switch or a career break in 2021, clients exiting Australia and switching tax residency status in 2021 etc).

8.Deferral OR bring forward of discretionary income

Defer discretionary income until after 30 June IF your circumstances will become favourable in the 2020 FY and vice versa e.g. maternity leave, imminent retirement, changing tax residence out of Australia, triggering capital gains (contract dates on disposal contracts) etc & vice versa

9. Share investors (capital account) – non-discountable capital gains

Consider pre 30 June disposals to book square against non-discountable gains triggered in the current financial year.

10. Share investors (capital account) – general CGT discount

Consider pre 30 June disposals which maximise the general CGT discount.

11. Employees with ESS interests in Australian listed employers

Consider points 10 & 11 above in addition to the 30-day disposal rule. Review your vesting schedules and enter into auto sale facilities with your employer/broker where appropriate.

12. Employees with ESS interests in foreign listed employers

Consider points 10 & 11 above in addition to ensuring that any foreign tax withheld is actually paid as soon as possible for Foreign Income Tax Offset purposes. Note: this one is complex. Please call Chris Bloxham (0414 985 724) to discuss before taking any action.

13. All capital account investors

Consider points 10 & 11 above along with optimal utilisation of carried-forward capital losses.

14. Property investors – interest in advance

Start interest in advance paperwork/authorisations/elections with your mortgagees NOW to make sure all payments are irrevocably committed before 30 June.

15. Property investors – ghost town Division 43 deals

The approach promoted by ‘ghost town’ Division 43 deals with caution. Please call Chris Bloxham (0414 985 724) or seek the opinion of a quantity surveyor before signing contracts.

16. Investment property depreciation

Please arrange for a Property Tax Depreciation Report as generally this will allow you to claim the maximum amount of depreciation and building write-off tax deductions on your investment property in Australia.

17. Defer investment income & capital gains

If possible, arrange for the receipt of Investment Income and the Contract Date for the sale of Capital Gains assets, to occur AFTER 30 June 2020. The Contract sales date is generally the key date for working out when a sale occurred, not the Settlement Date.

18. Higher-income employees with deductions or losses – PAYG variations

For PAYG earners with significant deductions or tax losses e.g. some property investors, returning expats with carried forward tax losses for utilisation in the 2020FY or the 2021 FY, call Chris Bloxham (0414 985 724) as soon as possible to consider putting a PAYG variation in place for your 2021 payments to capture the first pay cycle after 1 July 2020.

19. Private Health Insurance

If your taxable income exceeds $90,000 as an individual or $180,000 as a couple or you are 30 years of age and older, you should have complying private health insurance for all family members otherwise you may become liable to additional Medicare levy called the surcharge.

20. Tax deductible gifts

Make tax-deductible gifts before 30 June in the name of your family group’s highest income earner. Note: only gifts to registered Deductible Gift Recipients (“DGR’s”) qualify for a tax deduction.

21. Lodge your return early

If you are due a refund! This is your money, and it has real time value, so is better served to be in your pocket. Keep good records and lodge your return as soon as possible after year-end (30 June) every year to avoid paying penalties. Then invest or spend the money!

22. Keep records for efficient business management

In the event of an ATO review or audit, you will be asked to provide sufficient and relevant support including documents to substantiate the claims made.

Please ensure you have documented relevant records such as sales receipts, expense invoices, bank statements, credit card statements, lists of debtors and creditors, employee records (wages, super, tax declarations, contracts), vehicle records, logbooks, stock take listing, and asset purchases.

Contemporaneousness is supreme!

We hope you found some helpful hints and tips to consider leading to the end of every financial year. Please call us at Solve Accounting to discuss any of the above tax strategies and how they might apply to benefit your financial life.

What are Franking Credits? How do Franking Credits work?

The word Franking Credits or Franked dividends might sound unfamiliar to you, but it caught many Australian eyes during the 2019 Federal election. Before we dive right into what Franking credits are and how do franking credits work, let’s brush up on some basics.

One of the few business methods to raise capital is by listing shares on the stock market. However, money always comes at a price. When individuals like yourself invest in these shares, the company cuts you a small slice in the ownership pie. Woohoo! You can now officially become a part-owner of Tesla Inc. After investing in those shares, you will be officially recognised as one of the many company’s shareholders. All companies reward their shareholders with a portion of their profit, and this is known as Dividends.

The profit a company makes is taxed, generally a flat 30%, and the left-over profit is shared amongst shareholders as Dividends. However, dividends are categorised under passive income, and you are required to pay tax on the income you make. This basically means that the money you receive from the company you invested in is double taxed, and this is where Franking Credits come into the picture.

Franking Credits and How do they Work?

A dividend paid by an Australian company from their after-tax profits is called a ‘fully franked’, and the tax paid by the company on your dividend is known as ‘Franking Credits.’ For instance, you have received a dividend worth $700, and this is the slice of the net profit after tax.

Assuming the corporate tax rate to be flat 30%, the tax for the dividend you just received is $300. This will be already paid by the company on the $1,000 in corporate profit derived.

Along with the $700 in cash, you also receive a notice that labels the $300 as ‘Franked Credits.’ The sum of the dividend and Franking Credit is known as the ‘Gross Dividend,’ which is worth $1000.

Continuing with the numbers from above, you are now required to pay tax on the gross dividend. Now, let’s assume that the tax rate for personal income is 19%, and this means that you have to pay $190 for the dividend you just received. This will result in $490 being paid as tax for the dividend you received in a traditional taxation system. This results from double taxation and the ‘Franking Credits’ or “imputation” system that exists solely to prevent this specific scenario.

The ‘Franking Credits’ in your gross dividend will act as a tax credit. The practice of using Franking Credits as tax credits is known as “claiming Franking Offsets.”

Assuming the company tax rate to be 30%, the dividend you received will be tax-free if the tax rate for your personal income is also 30%, as you can simply offset the income tax on your dividend using the tax credit from the Franking Credits.

Moreover, if your personal tax rate is 46%, you are only required to pay 16% “top up tax” on the dividend, as the remaining 30% is already paid in the form of the tax credit. This system was established in 1987.

If we continue with the earlier example, the income tax to be paid for the $700 dividend is $190, and now you can deduct this using the Franked Credits, which is $300, and you will still be left with $110 of excess credits. This extra credit can then be used to offset tax on other tax levied on taxable income, or the excess credits can be filed for refund with the ATO if there is no additional tax to be paid on the taxable income. Hence, with this system, the issue of double taxation is resolved.

Another Example for Dividend and Franking Credits

The Australian Tax Office decides the income tax rate for every individual based on their income. Australian residents with income less than $18,200, or students, or low-income retirees are exempt from income tax. Franking Credits will be beneficial for these individuals, as they can file for a 100% refund of the Franking Credit as they have no tax to offset, resulting in the government receiving no tax from the company or the individual.

Unfranked Dividends and Partly Franked Dividends

Unfranked Dividends are basically dividends with no tax credit attached to them, which arises when the company makes profits. There is no tax levied on it and therefore no credits in its franking account to impute on a distribution. Now, how can a company make a profit with no tax being imposed on it? This type of profit is gained from the sale of assets with no tax levied on them or overseas earnings as the company does not pay tax in Australia. Hence, the dividends being distributed without any tax credits attached.

When a company declares 30% company tax on a ‘part’ of the dividend, this is categorised as a partly franked dividend. For instance, the company declares 30% tax on only 75% of the dividend, but not 25% of the dividend. In this case, you will receive more dividends with a lesser tax credit compared to a fully franked dividend.

These three types of dividends might get your head spinning, and you might wonder which one of the three will be beneficial to you. In the end, the tax paid and the amount that ends in your pocket will be the same. However, it will affect your investment strategy.

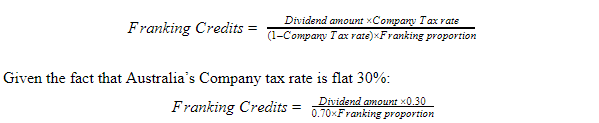

Franking Credit Formula

Franking credits are calculated using the formula:

45 Day Rule

In order to be eligible for franking credits, you are required to hold the shares “at risk” for 45 days, and this excludes the purchase and sale date (effectively 47 days). The shares are to be:

- Purchased before the ex-dividend date.

- In your possession in the ex-dividend date.

In the end, the world of Franking Credits might sound complicated but is easy to comprehend and more beneficial for you as more money will be available to you for future investments. The Franking Credits system successfully eliminates double taxation and has the potential to be followed in other countries in the following years.

How to Find an Accountant for Your Business

Accounting is an invaluable aspect of your business and business management, which means that you need to find an excellent accountant, to not only navigate the ever-changing tax laws’ maze but also to maintain critical financial records and offer sound financial advice about what you need to do to manage and gradually grow your business.

With a good accountant, you won’t have to worry about PAYG, BAS, or GST taxes, hence searching for the most qualified accountants.

But there are many accountants in the country today, and your first account may have disappointed you more times than you can take. So, how do you make sure that the next accountant you settle on offers all you need and more?

If you started a new business and you are looking for the right accountant for you to start things on the right foot, what do you look for when choosing a new accountant?

How Do You Find an Accountant?

An accountant is more than an expert that keeps you informed on all tax matters and changes and why you have to pay more in taxes this year than the previous year. Essentially, the right account will guide your management process and help in ensuring that you make the right decision on how to manage your finances while growing the business.

Whether you are looking to bring in new partners, purchase or lease a new commercial space, change the business structure, expand, or sell shares, an accountant is a person you need to know whether those ideas should be implemented or not. By analyzing the business’ past, present, and using future projections, an accountant gives you sound business advice.

Your accountant will also tell you how certain moves will affect the amount of tax payable and your business’ growth rate.

If you run a business, but you don’t have an accountant, you really are running the business on borrowed time, and that could be the reason for the business’s poor performance.

To find a good accountant, here are some of the basic steps you could follow.

- Referrals

The best way to find the right accountant for your business is to ask friends in business or other business people about their accountant, specifically, if they are satisfied with the services offered by the accountants or the accountancy firms they are working with.

You could look for referrals from the internet or the Yellow Pages if you didn’t find worthy referrals from your circles. When scouting for the best accountants, it’s a good idea to settle on the accountants with previous experience in service delivery in your industry. You’d want to come up with a relatively long list of prospective accountants to easily find your best fit.

- Call and interview about five accountants from your list.

Next, you need to shortlist the candidates that seem like they could be good fits for your business.

In the phone interview, ask about their education and certifications, and also their experience in your industry. You could also check with accountants’ professional associations to check the validity of the stated qualifications and for information about their character. Outstanding disciplinary issues, for example, tell a lot about the accountant’s character.

From this interview, you’ll easily narrow down the list to 2 or three accountants with that you can hold face-to-face interviews.

- Phone/Video Interview

For this interview, create a shortlist of questions that you’ll ask the prospective accountant. These questions will including their billing rates and how they determine their rates, their preferred communications channels, and their overall accessibility, and you could also ask them what they’d charge for basic tax returns for your company using an example from the previous year or a rough estimate. You’ll also ask and confirm their experiences in your industry, if they’ve worked in other countries (if your business has expansion plans to international markets, etc.

- Meeting prospective accountant chosen.

To gauge how well you’ll be able to work with the last one or two prospective accountants, you might want to schedule a face-to-face meeting. This meeting is important because it helps you gauge if you will be able to work with the accountant(s) or not, how comfortable you are with them, how well you communicate with each other, and if they really are who you want to run your business’s accounts.

What to look for when choosing an accountant?

At the end of the day, your business accountant is more than a tax preparer; they can help you come up with a definite blueprint to guide the future of your business.

- Understand your needs

Businesses have different needs, and you may need an account for more than bookkeeping and tax management. So, you should choose the accountant with proven records of their ability to do more, specifically, for them to help you run the business in the direction of growth and success.

Besides the not-so-obvious roles, you need to list all the other services you expect the accountant to provide. If you need the accountant to do everything from handling business tax, VAT/GST, PAYE/PAYG, business taxes, basic bookkeeping, preparation of end-year accounts, and filing of tax returns, you should list all these services. Other additional services like auditing, peer lending, provision of investment advice, etc., must be listed on your list of requirements.

- Check qualifications

Check and ask for their education and professional qualifications. Ensure that the prospective accountant has the accounting qualification they claim to have. Also, make sure that the accountant is a member of reputable accounting bodies like ACCA (Association of Chartered Certified Accountants). You’d also need to decide whether you are looking for a CPA firm or an accountant.

- Check for the licenses

By now, you know that an account is only in a position to give you the best tax advice if they are a tax agent, and they can offer financial planning advice only if they are accredited and licensed; and if they have the Australian Financial Services License. An alternative to the license that is acceptable would be a situation where the accountant is an authorized representative of a licensed accountancy firm or individual license holder.

In addition to licensing and accreditation, you also need an accountant who is appropriately qualified, with professional indemnity insurance.

- What kind of services the accountant offers

In line with making sure that the accountant is capable of meeting your needs, you need to confirm the services they provide. Is the accountant experienced in your line of business or the types of services you provide?

If you are looking for an accountant to take care of business tax, GST, PAYG, bookkeeping, preparation of annual financial documents, as well as auditing, credit management, trading internationally, investment advice/management services, etc., you’d want to look at the list of Accounting Services that the accountant claims to offer.

- Find a specialist

Depending on the size of your business and the type of business you run, you may find that you need the services of not just any accountant but a professional accounting adept in specific areas of business accounting.

The main specialties include bookkeeping, tax filing/ tax planning, auditing, advisory, and accounting. If you are looking for specialty services, find an accountant with a proven track record showing their ability to provide the service you are keen on.

Other specialty services offered by accountants include management consulting, business valuation, information system services, forensic accounting, etc.

- Consider location

Some businesses call for the hands-on and active involvement of an accountant. For these businesses, an accountant must be willing to visit the business location frequently or even work in-house. This is a common feature for large corporates and businesses that handle a lot of physical stock. So, if your business needs an in-house accountant or an accountant you can meet with on short notice, you should find an accountant based locally.

With cloud accounting, the location shouldn’t matter. However, there are situations where the location matters because you won’t be able to collaborate using any of the online/advanced communication channels available.

- Experience

You are most likely a small business, which means that you need an accountant with experience in running finances for small businesses. Your budget could also be too small for you to afford the services of the big accounting firms, which is why you’d be better off with an account or an accountancy firm like Solve Accounting with experience working with small businesses.

- See what other clients have to say

Before you settle on an accountant, check online reviews of their services. You could also use online forums or social media to determine whether you should trust the accountant or not. Your social networks are also incredibly helpful.

So, check out who they are connected to, how they talk about their profession and the services they provide, whether they’ve been recommended by their past clients, and the experiences of previous clients. The online space is essential if you are going to find an accountant in Sydney.

- Fees and Billing

What are the accountant’s fees, vis-à-vis the services they provide? Do other clients claim to get value for money for the services provided?

How do they charge? Most accountants charge by the hour, which means that it may not be the business move to have the accountant come in to do the data entry work. To ensure the best value for your money, choose accountants who are proactively working on saving your money through the use of the best quality accounting services or working out ways that you can cut down operational costs on.

- Software used

Accountants often have preferred accounting software that they use. Since the accountant may be in your company for many years, you might want to switch to the type of software they use/vice versa to avoid data-sharing issues. For easy accounting, opt for the accountant that uses the software you use, or with the option of using the same accounting software that you use (most accountants use more than one software).

Conclusion

A good accountant will help your company grow. Since the accountant is intimately involved with all the operations of your business, you need an accountant who checks all the important boxes above. You also need to find an accountant you trust and one who will be there when you need them.

What is a BAS, and Do I Need to Lodge a BAS ?

Running a successful business pushes you to put all your skills and abilities. You will learn so much on the job, make mistakes, have big wins, take big losses, and you’ll be forced to take risks you never thought you’d ever have to take.

While some of the calculated business risks payoffs, there are risks you should avoid at all costs. One such risk is being on the wrong side of the law, specifically, not having your taxes and books in order.

There are numerous tax obligations that are tied to your business from the moment you register the business, and you need to learn what they mean and how to file for such obligations and pay liabilities within the stipulated timelines and before the deadlines.

One of these obligations is the BAS tax obligation, and if you are a small business owner, BAS is one of those small business obligations that you need to stay on top of.

At the same time, you need to understand what BAS is and what it entails because some businesses are required to lodge BAS, and others aren’t.

So, let’s get started.

What is a BAS?

BAS or the Business Activity Statement can be defined as a form or statement issued quarterly or monthly for reporting of your business’ tax obligations, for example, Pay As You Go (PAYG) instalments tax, Goods and Services Tax (GST), fringe benefits tax (FBT), PAYG withholding taxes, Luxury Car Tax, as well as the wine equalisation tax, among others.

Do you need to lodge a BAS?

Although the Business Activity Statement is a requirement for most small businesses, not everyone is required to lodge BAS. Generally, the nature of your business determines where you need to lodge BAS or not.

Essentially, you are required to lodge BAS only if your business is registered for GST, which means that if you are a new business that isn’t registered for GST yet, you wouldn’t have to lodge BAS.

That said, GST registration for businesses is required for businesses whose gross income equals or exceeds $75,000 (but excluding GST value of 10%).

So, should your business be registered for GST during its initial registration?

Well, it’s not necessary to register your business for GST during the business’ early stages, but you should be ready to register for GST and lodge Business Activity Statements once your business starts bringing in more bacon. Registering for GST is a legal requirement once you gross $75,000.

Confused and unsure about how to start lodging BAS? Don’t worry because, in as much as you are required to know these things, your relevant Australian Taxation Office (ATO) will inform you about when you’ll be expected to lodge BAS. You will receive this notification when registering your business for GST and the Australian Business Number. Often, the ATO sends you the BAS automatically before the lodgement date. Once they send the notification, you’ll be required to complete and lodge it before its due date.

Besides the GST pre-qualification and submission of lodged BAS, you also need to know your business type before BAS submission. This is crucial because the requirements for BAS submissions will vary depending on your business’s structure. This means that the requirements for limited companies will differ from those of sole traders or partnerships, etc.

When do you need to lodge your BAS?

If your business isn’t registered for GST, you won’t have to worry about BAS just yet, especially if your gross income is still low. But if your income is above $75,000 and you are registered for GST, you will be required to lodge BAS.

It’s important to note that registering for GST is an option, but once you cross the threshold, you will need to register and lodge BAS from your GST sales.

For GST registration, there also is a threshold that you are required to meet, depending on the type of business you run. Here are the requirements that your business must meet to qualify and register for GST.

- Your annual business income/ turnover must be more than $75,000

- If you run a not-for-profit business, you’ll have to register for GST once the annual turnover recorded is over $150,000.

- And if you are a Rideshare or a taxi driver, you are legally required to register for GST from the day you start the business.

What if you miss the set threshold? For businesses or companies that miss the threshold, you will be required to backdate your registration for compliance purposes. But backdating isn’t enough, and you’d have to pay the total GST owed on the business goods/ services from the date that you crossed the threshold.

With GST basics out of the way, when are you required to lodge BAS?

BAS is tied to your GST registration, and you are required to lodge BAS either monthly or every quarter. As a tool that allows for reporting and payment of GST, PAYG instalments, or PAYG Withholding taxes, you need to lodge your BAS before the deadline for tax reporting and payment.

The frequency of lodging BAS is tied to your GST turnover. Below is a more specific breakdown of how to lodge BAS and the frequency of lodging the statements.

- For Quarterly BAS reports, your business should have a turnover below $20 million. Also, you’d have to lodge this quarterly BAS if your ATO hasn’t sent you a notification yet.

- For the BAS to be lodged monthly, your business should have a recorded turnover of at least $20 million.

- And for you to lodge BAS annually, you’ll be required to first register for GST voluntarily, and your business’ annual turnover shouldn’t exceed $75,000 or $150,000 if you run a non-profit.

To ensure that your data is recorded correctly, you’ll need the help of a registered BAS or tax agent.

Quarterly BAS Reporting

Even with these options, most businesses opt to lodge their BAS quarterly. For the BAS lodged quarterly, the specific due dates for lodging are as follows:

- The deadline for Quarter 1 (July, August, and September) is 28th October.

- The deadline for Quarter 2 (October, November, and December) is 28th February.

- The deadline for lodging BAS statements for Quarter 3 (January, February, and March) is 28th April

- The deadline for lodging Quarter 4 (April, May & June) BAS statements is 28th July

If you lodge your BAS online, you will be eligible for an extra two weeks during which you can lodge and pay the quarterly BAS.

Also, the later lodgement plus payment due dates aren’t applicable to the 2nd quarter because of the one-month extension provided.

Monthly BAS Reporting

As mentioned above, you can lodge your BAS monthly if your gross GST turnover for the month is at least $20 million. You’ll need to report and pay your monthly GST and lodge your BAS online by the 21st day of the next month. So, BAS for February would be due on 21st March.

For schools or associated institutions, you will be granted a deferral automatically for your December BAS, but you’ll need to lodge the deferred BAS by 21st February.

Annual BAS Reporting

The due date for the annual BAS reporting is 31st October. But if you aren’t obligated to lodge your tax returns, then the due date for reporting and paying your annual BAS is February of the following annual tax period.

As mentioned above, you should use a registered tax agent or BAS agent for the reporting. Also, the dates may differ, but it is a good idea to confirm with your agent ahead of time.

How do you change your business’ BAS reporting and payment cycles?

You may be able to change the frequency of lodging and paying BAS depending on circumstances.

If, for example, you wish to change the current BAS reporting and payment cycle, you’d want to do that early in the BAS lodgement period. So, to change the lodgement and payment period from the first month of the quarter or even at the beginning of the financial year, you can do that by starting that change immediately (the keyword here is EARLY in the cycle). Failure to do this means that the new cycle takes effect at the start of the next year or quarter.

What happens if you don’t lodge your BAS?

Understandably, there are times when you won’t be able to lodge or pay your BAS by the due date. If you anticipate delays or a complete inability to pay your BAS on time, you should talk to your BAS agent or your ATO office as soon as possible and before the deadline for the best remedies.

Basically, you are obligated to lodge and pay your BAS before the due dates, and this means that the inability to beat the deadline will attract some penalties. To avoid being penalized for the lateness in lodging and paying BAS, you could lodge in time (if you are in a position to), then lodge later. Even if working with a tax agent, your ATO should be contacted in case you are unable to lodge and pay BAS.

Note that we recommend lodging BAS even if you aren’t able to make the payment by the deadline because once your BAS is lodged, a talk with your ATO would allow you to enter into a more flexible payment plan. You could use the online payment plan estimator to work out an affordable payment plan.

The payment plan calculator also helps you determine how quickly you’d pay off the tax debt. The calculator calculates the total interest charged on the outstanding tax debt. The interest charged on the tax debt is called the general interest charge (GIC), and it’s applicable to any tax/ BAS-reported tax not paid by the deadline.

What’s the Penalty for failing to lodge BAS on time?

The penalty for failing to lodge BAS on time is referred to as the Failure to Lodge (FTL) on time penalty. This penalty may be applied if you miss the deadline for lodging tax returns, BAS reports, or statements (or even both).

The FTL penalty charged is calculated differently, depending on the size of the business.

- If yours is a small business entity, the FTL penalty will be calculated at the specific rate of One Penalty Unit for every 28 days that the tax return or BAS is overdue; to a maximum of 5 penalty units. The value of the penalty unit as recorded from 1st July 2020 is $222.

- For medium businesses, the FTL penalty will be multiplied by two. Note that the medium business entity is the business run by a medium withholder for PAYG’s withholding tax purposes or entities with current GST income or assessable income that is more than $1million but less than $20 million.

- The FTL penalty for the large entities will be multiplied fivefold. Large entities refer to the large PAYG withholders with a current GST turnover or accessible income over $20 million.

- Lastly, you have the global entities. These entities will have their base penalty amount multiplied by 500.

To avoid penalties, Solve Accounting offers comprehensive taxation and Accounting Services that ensure all the information on your BAS is accurate and lodged on time.

How do I lodge my BAS?

This is the other crucial bit about BAS.

There are different options for lodging BAS (as well as GST). These options ensure easy lodging of BAS and also ensures that you don’t miss the deadline and pay penalties/ high-interest charges.

Most businesses opt to lodge their BAS online.

How to lodge BAS online

If you wish to lodge BAS by yourself, the online option would be the most ideal for you.

Businesses that are allowed to make their quarterly BAS lodgement online are often eligible for concessions, and if you are lodging BAS without the help of a tax/ BAS agent, you will have two extra weeks to lodge and pay your BAS.

Here are the simple steps for lodging BAS online:

- Online Services (specific) for sole traders and individuals (this is accessible via MyGov). This platform also makes it easy for you to manage taxes plus the super from one place.

- The Business Portal – this is a secure ATO portal/ website set up for easy management of all your business tax affairs online.

- SRB-Enabled software – this software makes for easy and secure BAS lodgement from your payroll, accounting, or financial software. This software is often integrated with software solutions tailored for use in specific industries.

Lodging BAS via your BAS or Tax agent

For outsourced BAS services, you’ll need a registered tax agent or a BAS agent to take care of your tax matters, the agent could lodge your BAS for you. The agent could also make the payment for the business under your account using selected electronic channels.

If you choose this option, you should make sure that you can view all your statements from your business’ MyGov Inbox. You also need to make sure that you still have access to your business activity statement via the business portal or MyGov.

ATO has a list of registered agents that you could work with, meaning you don’t have to worry about unregistered/ unscrupulous agents handling your finances.

How to report NIL BAS

If your business doesn’t have any statements to report for that period and you’ve registered for GST, FBT, PAYG, etc., you’ll need to lodge the period’s BAS as NIL.

For the ‘nil’ BAS recording, you have the option of making the nil record online or by phone. To lodge nil BAS by phone, you’ll use the number 13 72 26, which is a telephony automated service that’s available 24/7. You’ll need the Business activity statement Document Identification Number (DIN) to simplify the nil lodgement via phone.

Lodging BAS by Mail

The third option for lodging BAS is via mail.

To lodge your BAS via mail, you have to mail the original and accurately completed BAS. You’ll mail it with the pre-addressed ATO envelope (this is given as part of the BAS documents’ package for your business). In case you make a mistake or miss some details on the paper ABS, you could use white-out to make the relevant changes.

If lost or if you haven’t received your paper BAS yet, you could obtain a copy of the paper ABS by calling 13 28 66.

That said, you wouldn’t have to mail the paper BAS if you are lodging BAS online.

So, how will you receive your statements?

Your BAS statement will be sent via the same channel used to lodge BAS. So, your statements will be in your Business Portal if you lodge the BAS online; and it will be sent by mail if you lodge BAS via mail.

What are the BAS Requirements?

To qualify for BAS, there are some requirements that you need to meet. But the most important thing to keep in mind is that you qualify for BAS if you are obligated to pay the following taxes – GST, PAYG for tax instalment, PAYG for tax withheld, fringe benefits tax (instalments), luxury car taxes, fuel tax, and wine equalisation taxes.

How Often Do I Have To Lodge a BAS?

You can lodge BAS monthly, quarterly, or annually.

Conclusion

If you have a small business and meet the requirements above, you should lodge BAS. If you aren’t sure what to do and how to go about BAS, the simple guide above should give you a good headstart.

Expats and COVID-19 on Australian Tax Residency

The ongoing COVID-19 pandemic has played havoc with international travel and employment arrangements around the world. Many Australians are now stuck outside of the country or have returned home temporarily.

On top of this, other Australian citizens and permanent residents have been banned from leaving the country and are stranded. Will the expats who have come back to Australia temporarily due to the coronavirus crisis be allowed to continue working with companies outside of the country?

This is a daunting question for many people and can give rise to uncertainty when it comes to tax residency and taxation of foreign employment income.

It is possible that prior to the COVID-19 pandemic most expats did not consider themselves to be Australian residents for tax purposes. However, does their return to Australia, temporary as it may be, change that status? If they continue to work remotely for a foreign employer, will they be taxed in Australia?

The official guidance on these questions in Australia is fluid and continues to change. While the COVID-19 pandemic has created a range of unique and unusual circumstances far beyond anyone’s control, taxpayers should still seek to understand their tax status and ensure they proactively prepare for any Australian Taxation Office (“ATO”) enquiries.

Where you have experienced the following circumstances, you may need to consider your tax status in more detail:

- Your arrangement with your foreign employer or business has changed (e.g. you have a foreign employer remote work arrangement)

- You have begun working temporarily in Australia whilst remaining a foreign tax resident

- Your housing or accommodation arrangements have changed

- You are considering staying in Australia beyond the original “lockdown” period

Each of these factors may indicate a change in your residency status or the taxation of your foreign income. With all these different unknowns, it would be worth the effort to gather and generate evidence around your intentions and whether you are a tax resident or not, given ATO scrutiny in this area.

What Is Tax Residency?

An individual may be considered a tax resident of Australia in the first instance taking into account many factors, including employment, living arrangements, family, location of assets, personal relationships, memberships, health cover, intentions to reside in Australia, and so on.

Further, an individual can be automatically considered an Australian resident where they have a “domicile” in Australia or have physically been in Australia for more than half of the income year.

To be clear, the tax residency rules applied by the ATO differ from the criteria used by the Department of Home Affairs to determine citizenship. The ATO could consider you a resident even if the immigration office does not.

If you are an Australian tax resident, you:

- Must file an Australian income tax return with the ATO

- Must declare your income from all sources around the world

- Become entitled to the tax-free threshold, meaning that you don’t have to pay taxes up to a certain amount

- Will have to pay the Medicare levy (subject to the thresholds).

Alternatively, if you are not an Australian tax resident, you:

- Only pay tax on income that is “sourced” in Australia (note you may get relief from Australian tax depending on the country you are working in)

- Must file an Australian income tax return with the ATO if you have Australian sourced income

- Do not receive the tax-free threshold, meaning you are taxed on income from the first dollar

- Will not have to pay the Medicare levy

With many people now coming back to Australia – or unable to leave – because of COVID-19, the issue of tax residency and source is thrown up in the air.

Does Being Stuck in Australia Impact Tax Residency?

The ATO recently issued updated guidance on how it plans to approach tax implications for Australian expats living in Australia right now. The ATO has indicated that if you are a foreign resident here temporarily due to COVID-19, you will not become an Australian tax resident if you:

- Usually live overseas permanently

- Intend to return overseas as soon as you are able

However, if you end up staying in Australia or do not intend to return when able, you should review your residency status.

These guidelines are not binding on the ATO and the ordinary residency rules outlined above should still be considered on a case by case basis. Thankfully, the guidelines appear to indicate a common-sense approach to tax residency by the ATO considering the COVID-19 restrictions.

Foreign Employment Income

If foreign tax residents are temporarily stuck in Australia due to COVID-19, the ATO has indicated the following:

- Paid Leave – If you receive paid leave from an overseas employer whilst living in Australia, such as annual leave, the ATO will not consider it Australian income, and so you won’t need to declare it in Australia.

- Working Remotely – The ATO has indicated a ‘rule of thumb’ for remote working for 3 months or less will not be considered Australian-sourced income. A remote working arrangement that extends beyond 3 months will need to be considered carefully from an Australian tax perspective.

These indications are helpful to provide some clarity to Australian expats who have returned to Australia temporarily whilst continuing to work for a foreign employer. Given that the situation continues to evolve, the ATO will continue to update its guidelines as necessary.

* * * * *

If your foreign employment circumstances have changed due to COVID-19 and you are unsure how to apply the ATO guidelines, get in touch with your accountant or tax adviser to assist you.

The issues of tax residency and income source are complex and may differ based on your personal circumstances, so don’t hesitate to contact the experts.

Australian Federal Budget 2020-21: Key Takeaways

Below are some of the key takeaways announced in the Australian Federal budget for 2020-21. In the budget, many areas were touched upon. However, we have narrowed it down to the most significant measures that are aimed at taking Australia through this economic crisis and bounce back up as quickly as possible.

Reduction in Taxes

The tax burden will be reduced for many Australian citizens with over 11 million set to receive a cut of $47 per week. This will apply to high-income earners. Middle-income-earners can also expect a cut of $21 per week, with the previous budget tax cut rolling on for lower-income earners. In the Federal budget, there is also an increase in the upper limit of the 19% tax bracket, which will become $45,000. The 32.5% marginal rate will increase to $120,000 from a previous figure of $90,000.

Incentives for Employers

There has been a big focus on ensuring that jobs can be retained and that further opportunities can be provided. Youth unemployment, in particular, has focused on, since they are the demographic that has been hit hardest during this recession. The government has pledged funds of $200 per week for firms to hire youth. This incentive will apply for firms that take on young workers who had previously been on jobseekers. Additionally, the government will cover 50% of the wage for apprenticeships and traineeships.

Welfare Supplements & Educational Funding

Additional welfare supplements will include payments of $250 to pensioners, and an extension to job keeper payment support which will be extended to 28th March 2021. The Coronavirus supplement will also be extended to December 31st 2020. Educational funding will include a $1 billion injection into the university research sector. Additionally, there will be added funding for online short courses that aim to re-skill unemployed workers. A total of $299m will be given for universities to add 12,000 more places for the new year.

Funding for Small Businesses

The vast majority of businesses in the country (those with a turnover of less than $5 Billion) will be eligible for deductions involving the cost of capital incurred after budget night and used before 30 June 2022. Smaller and medium businesses will be able to benefit from expensing second-hand assets. Businesses earning between $50 million and $500 million will be able to expense assets that are valued at less than $150,000. NBN Co will receive $4.5 to ensure a smooth rollout of the 5G network across the country.

Investment in Healthcare & COVID -19 Treatments

Healthcare is set to receive significant investment in light of the Covid-19 pandemic. There will be packages set out for elderly Australians that are waiting for home care, and this will cost $1.6 billion. An additional $2.3 billion will be spent on investing in Covid-19 treatments and vaccines. A further $750 million has been pledged for Covid-19 testing and $171 million for respiratory clinics that are managing Covid-19 cases. $798.8 million will be given to the national disability insurance agency, and for the NDIS quality commission. There will also be a new tax exemption for granny flats where this arrangement involves an elderly individual or someone with a disability.

Funding for Infrastructure

There is also a range of pre-announced measures that deal with infrastructure, the environment, and energy budgets. The government has pledged to renew the Australian Renewable Energy agency by another ten years from 2022 at a total cost of $1.4 billion. $50 million will be spent on carbon capture that could help to cut down emissions. $67.4m will be budgeted for oceans and marine ecosystems. Recycling policies will receive $249.6 over the next four years.

Another large investment for the next four years goes to various infrastructure projects. In total, $14 billion will be spent on modernisations in each state and territory. This includes the Melbourne to Brisbane inland rail.

Superannuation Fund

Individuals will no longer need to create multiple accounts for these funds when changing employers. A new tool will be set up to help individuals monitor the performance of their funds.

Recommended Actions

We have devised a list of actions that you can take to save on your tax bill based on these takeaways.

- When you sell an asset, you might face tax issues in the future. This is due to the Federal Budget 2021 taking 100% of your proceeds and business income. This can result in businesses registered as a trust, sole trader, or a partnership that pays more tax than the benefit they received during the purchase.

- When a registered company purchases an asset of $100,000 against an offsetting profit, the tax for the same is calculated as $26,000. This essentially means that you have to repay $74,000 of the fund.

- You are not entitled to claims on Motor Vehicles

- Companies and trusts that benefit from Fringe Benefits Tax may have to pay a loan on cars, and this can be greater than the benefits received initially during the purchase. This is true for companies that purchased cars that cost more than $59,132, which is the max limit set for 2020/21.

- Banks will start to look at write-offs as the signal of loss, and such businesses may not receive a favourable assessment. So, to ensure the client’s serviceability is not affected, it’s ideal not to use personal and business lending options with instant asset write-off. Take any decision on this front after consultation with a financial expert. That said, we can help you with this by doing accounting and tax depreciation schedules.

- Chattel mortgage repayments can have a bigger impact on the serviceability of lending, including home loans and business lending. Ensure that you make timely purchases keeping in mind your current financial condition so that you are not impacted by the purchases. With our help, you can be better equipped to make the right purchase decisions.

Federal Budget Summary

The Australian budget is designed to get the country through one of the worst economic crises in their history. This new Federal budget is unlike most, and it is hoped that these measures will be enough to stimulate the economy. You will have seen a variety of costs that are being undertaken. Whilst some have been planned, many others have been forced due to the ongoing economic impact of the pandemic. It remains to be seen whether any of these measures may be modified in accordance with the ever-changing situation. We will keep you updated with any potential changes to the federal budget initiatives once they come into effect.